Conventional wisdom, dating back to the published work of Michael Porter, paints a simple picture - businesses can be categorized as either commodity or differentiated, each with unique characteristics that define the nature of competition and structure. The implication for the manager is that you need to choose a business model (commodity or differentiated) to align your management approach to one of two market realities.

Following this logic, the concept of a “differentiated commodity” business seems a contradiction in terms. Our experience suggests quite the contrary. In practice, most businesses are neither purely commodity nor fully differentiated, but hybrids - that is, where a meaningful percentage of products, markets, or customers served are commodity, with a second meaningful percentage being differentiated. A third portion is typically transitioning from differentiated to commodity. This split of commodity and differentiated segments is dynamic, tending toward a higher percentage of commodity segments over time. The pace of change varies considerably depending on the industry (e.g., the electronic materials case study describes an industry where change can be rapid) and how effectively a particular company manages its business.

To better understand and manage these differentiated commodities, management needs to address several critical questions.

Key questions

- What are the major drivers of value in a differentiated commodity business and how do they shift over time?

- What business models are suited to creating maximum value in a differentiated commodity industry? What are the common pitfalls to avoid?

- How should management design key elements of the business model, such as cost structure, technology and innovation, market and customer segmentation, M&A, investment strategy, and overall go-to-market strategy including offering and service levels and pricing approach?

- What organisational structure is best suited to managing a differentiated commodity? Do you need to separate into two businesses, creating two sales forces and customer service models, etc.? What are the primary metrics to guide the successful management of a differentiated commodity business?

This article is based on our experience working with companies looking to earn attractive returns in businesses which are not inherently the pure plays described in traditional management literature. We do not attempt to cover all the questions above in depth, but provide an overview of the first three.

Defining a differentiated commodity business

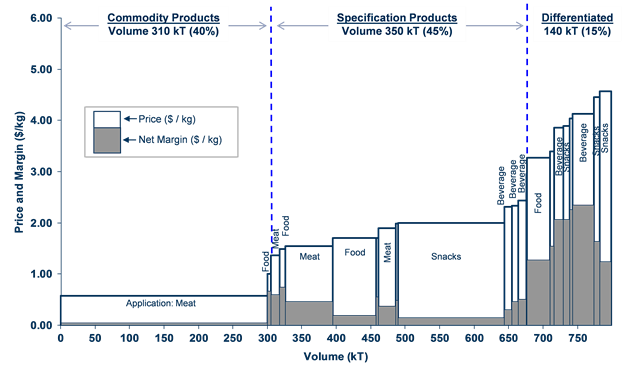

A differentiated commodity business is best understood by examining its value-added structure (price / volume curve shown in Figure 1). The food ingredients business depicted in Figure 1 is composed of three primary segments: a low-priced commodity segment where the product is used as a filler and there is virtually no product differentiation; a pseudo-commodity or specification segment where the product is used to provide specific nutritional benefits and needs to meet tighter quality specifications; and a differentiated segment where the applications (e.g., snacks, beverages) require higher quality and performance attributes which many producers cannot meet. As a consequence, the price premium for the differentiated segment is considerable.

Figure 1: Food ingredients market structure – illustrative example

The real economics of a differentiated commodity business are best seen by examining net margin realisation after deducting the cost to serve the market (production costs and the cost to support the customer pre- and post-sale). In Figure 1, net margin realisation is depicted as the grey shaded area inside each product line / application segment. The net margin realisation for each segment differs considerably, though it is clear that the bulk of the commodity volume produces very low net margins. The differentiated segment is the most profitable, representing more than 50% of the total margin, but only 15% of the market on a volume basis. The challenge for management is to sustain these price differentials and invest to grow the segment. The relative size of these three segments has changed considerably over time, with the commodity and specification segments representing an ever-increasing share of the total business.

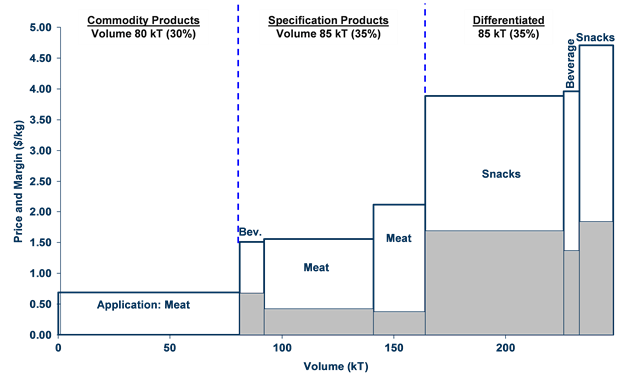

The value-added structure is often not the same across regions. Figure 2 shows that the performance of the commodity segment is particularly poor in North America. However, the differentiated product segment represents 35% of volume, 50% of revenues, and more than 60% of total net margins. In this case, competitive differences in the three main regional markets (North America, Europe, Asia) led to three related, but quite distinct differentiated commodity structures.

Figure 2: Net margin realisation vs. volume – North America

The Do's and Dont's of differentiated commodities

Do

- Match structural change in the business model to structural shifts in the industry—managing change ultimately sets you apart

- Target a low-cost supply position, the threshold requirement to serve both differentiated and commodity segments

- Plan on the current areas and sources of differentiation to decline over time

- Innovate to develop new differentiated products/ applications - key to counter the natural erosion of the differentiated segment

- Differentially allocate resources, such as new product development, technical service, and sales resources based on customer willingness to pay

Don't

- Manage the business as a purely differentiated model - not sustainable. Presume you can change as fast as change happens - need to proactively adapt model to changing market and competitive landscape - a holistic change program is key

Life cycle of a differentiated commodity

Differentiated commodity industries evolve in similar fashions but have different starting points. Life cycle of a differentiated commodity

- Differentiated commodity businesses that over time tend to become more commoditised (see commodity polymers case study)

- Businesses that are largely differentiated that evolve into differentiated commodities (see electronic materials case study)

Review of selected case studies in managing differentiated commodities

The two case studies highlight the nature of the management challenges and models required to profitably participate in differentiated commodity industries.

Electronic materials

The industry leader in this traditionally highly profitable business, with a broad portfolio of generally differentiated products sold into the fast-change electronics market, began to experience significant declines in performance. A fairly marked and rapid shift occurred in the performance of its core product line, with not only cyclical volume declines but falling prices. Structural changes were underway. Pricing pressure from a concentrated customer base and better positioned, low-cost Asian competitors were changing the business dynamic, effectively commoditising its largest and historically most profitable product line.

Management’s initial response was a range of mostly incremental measures (although they may have seemed more dramatic at the time) to reduce SG&A, lower the manufacturing cost structure, and enhance / streamline the product mix. In the end, these were not sufficient to keep pace with shifts in the market and competitive environment. Conditions got worse during the subsequent economic downturn, when volumes fell quite dramatically and prices, once again, fell rapidly.

Management implemented more dramatic reductions in SG&A, further rationalised the product line, and reduced supply chain costs wherever feasible. These moves helped the business pull through the downturn, they did not put the business back on a path to cost-of-capital returns.

The company decided to take a fresh look at the business. Segmenting it into commodity and differentiated product lines highlighted the drivers of performance and the dramatically different segments. While the differentiated product lines were able to limit margin erosion and earn their cost-of-capital through the cycle, the major commodity and pseudo-commodity products’ performance deteriorated markedly.

The assessment highlighted some fundamental lessons that would guide its new plan of action. A principal lesson was that to sustain or re-establish their leadership position required a fully competitive, if not industry leading, low-cost position. Second, management concluded that their traditional sources of advantage—scale, product quality, and strong customer relationships—were no longer sufficient. Third, the legacy of very high margins driven by a leading product line had encouraged investments in poorly performing (largely unprofitable) product lines and applications in the pursuit of growth. As a consequence, the new management embarked on a program to drive more fundamental changes tied to these three lesson to support sustained performance improvement.

Commodity polymers

The structure and competitive dynamics of the commodity polymer industry, which includes businesses such as polyethylene, polypropylene, PVC, and polystyrene, have changed markedly over the past few decades. Change has been driven by the entry of new players, shifts in technology, changes in the application profile, sizable swings in feedstock (energy) costs, and the response by existing participants in reaction to these changes. In our experience with the commodity polymers industry, we have seen three primary models. Two models generally create value and one has consistently destroyed value.

Legacy leaders in commodity polymers had models typically founded on three pillars: advantaged technology, a broad product offering and application footprint, and scale. A major force for change was the emergence and growth of the relatively pure, low-cost players with feedstock advantages (e.g., in Saudi Arabia and Western Canada), scaled facilities, largely standardised product lines, and limited participation in differentiated segments. These players proved to be formidable competitors, exerting pricing pressure on the commodity and quasi-commodity segments of the market.

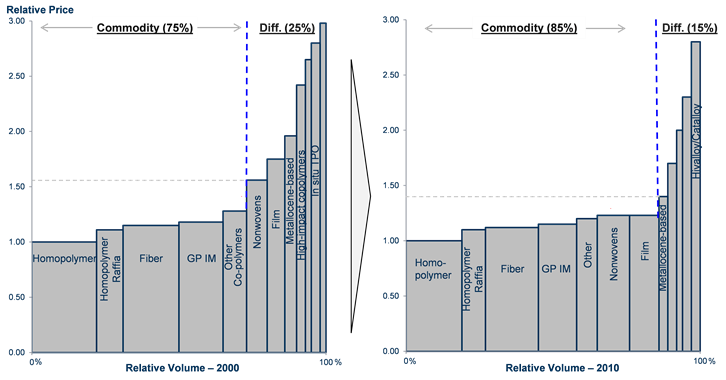

In response, the legacy leaders typically took one of two paths - stay the course with continued pursuit of what propelled them to leadership (i.e., technology, product offering, and scale), or holistically adjust their models to the reality of the growing commoditization of the business. The first group (comprised largely of major diversified chemical companies) struggled to remain competitive. Over time, with growth, the proportion of the business represented by differentiated products shrank, and so too did the premium associated with these products, which effectively commoditized the businesses. Figure 3 below illustrates the commoditization of the polypropylene industry over about a 10-year period. It highlights both the relative decline in the size of the differentiated segment and the fall in price premiums. The pace of commoditization of the business varies based on changes in process technology, specifically technology that lowered the cost not only of producing the commodity product lines, but also many of the previously differentiated ones that fetched a sizable price premium.

The companies that succeeded in the transformation not only adjusted their cost structures to the effective commodity nature of the overall business but also systematically invested in innovation to drive new, more differentiated products and to provide a tailored approach to selected segments tied to customer needs.

Figure 3: Flattening price curve over time – polypropylene

Conclusion

Getting it right in differentiated commodities is about recognising the value added structure, having insight into varying customer needs and market pressures, and adjusting the model to perform in this environment. While traditional competitive strategy paints a black and white world of commodity and differentiated businesses, our experience suggests that most industrial businesses are a combination of the two - in essence, differentiated commodities. Moreover, these differentiated commodities are dynamic, with competitive forces transitioning products and applications toward commodities. Managing the inherent differences between the two pieces of the business is no easy feat, and many companies don’t get it right or move fast enough to keep pace or stay ahead of change. To succeed, management must put in place a model that, above all else, is focused on building a low-cost position through asset footprint and supply chain efficiency, while tailoring investments and customer support only for those segments that provide sufficient differentiation.

Fundamentals of managing a differentiated commodity

- Know the competitive market structure and be realistic on how it might evolve

- Understand your competitive position and its underlying economics

- Get the cost structure right - asset footprint and supply chain efficiency is the foundation

- It’s one business that needs to be adapted over time embracing a holistic view of the industry and the target business model